What type of entity should I use?

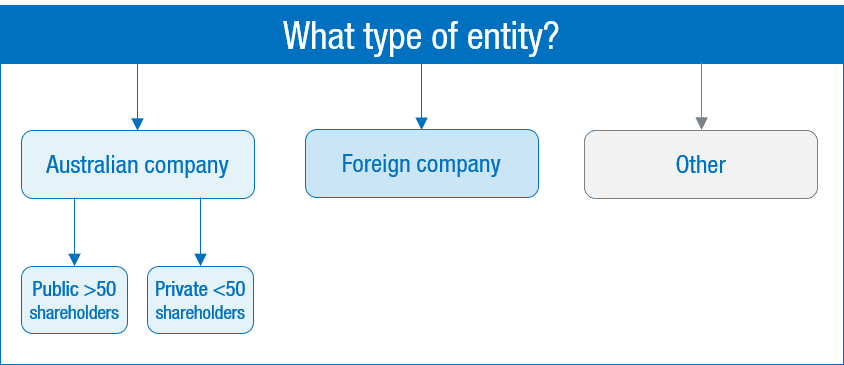

As a foreign investor, there are several important considerations when deciding how to establish a business in Australia. Although Australia has various types of structures available for establishing a business, the most common types of entities used by foreign investors operating in Australia are a private company (Pty Limited), or a branch of a foreign company. With each different type of entity comes different legal and tax implications that investors need to consider.

Establishing an Australian company

The most common structure used by foreign investors to conduct a business in Australia is an Australian private company, that is, a ‘Pty Limited’ company.

An Australian private company is a separate legal entity that is required to be registered with the Australian Securities and Investments Commission (‘ASIC’). When registered, each company is issued with a unique Australian Company Number (‘ACN’).

A private company:

- Is limited to 50 non-employee shareholders.

- Cannot engage in fundraising activities.

- Must have at least one director who resides in Australia. If a Secretary is appointed, the Secretary must also reside in Australia.

- Must have a registered office in Australia and appoint a public officer;

- has various annual reporting obligations. However, these will vary depending on the size of the private company.

- Can be 100% foreign owned.

- Has a minimum number of one shareholder/s and no restriction on the number of shares that can be issued.

- Is governed by the Corporations Act 2001 (Cth) (‘Corporations Act’).

The restrictions on shareholders and fundraising do not apply to a public ‘Limited’ company. A private company can be converted to a public company if needed.

Provided all the information necessary is gathered, an Australian company can be registered with ASIC within one business day. Additionally, incorporating an Australian company does not require an attorney.

Establishing a foreign branch

A foreign company may choose to carry on a business in Australia itself. This is known as establishing a foreign branch.

Where a foreign company chooses to carry on a business in Australia itself, it must be registered as a foreign company under the Corporations Act. The foreign company must apply to ASIC to register an Australian branch. Upon registration, a unique Australian Registered Body Number (‘ARBN’) will be provided to the Australian branch. The registration process can take up to four weeks to process, provided all the necessary documentation is provided to ASIC.

As with Australian companies, a foreign company establishing a branch in Australia must have a registered office in Australia and must appoint a public officer. The company must also appoint a local agent, responsible for the company’s compliance with the Corporations Act.

Once registered as an Australian branch, the foreign company must lodge its annual Financial Statements with ASIC and comply with specific reporting requirements.

Notably, operating though an Australian branch does not create a separate legal entity, as is created when a private or public company is incorporated.

Alternatives available

Other types of structures are available in Australia and may be appropriate in particular circumstances.

A trust is a common form of business structure used in Australia by smaller, privately owned businesses.

Trust income is generally taxed in the hands of the beneficiaries each income year.

A trust is governed by common law and contract law in Australia. Establishing a trust does not require an attorney.

For foreign investors, trusts (mostly unit trusts) are generally used for property investments in Australia.

There are also specific entity structures available for venture capital investments and managed investments.

What registrations will I need?

The registrations required will depend on the type of entity. All Australian registered companies will have an Australian Company Number (ACN) whereas Australian branch operations will usually require an Australian Registered Body Number (ARBN). All entities operating a business will require an Australian Business Number (ABN).

There are also a variety of business and tax registrations which may also be required as a result of conducting business in Australia, such as registrations for:

- A Tax File Number

- Goods and Services Tax

- PAYG Withholding

- Fringe Benefits Tax, and

- Payroll Tax.

Corporate registrations

All Australian registered companies will have an Australian Company Number (ACN) issued by the Australian Securities and Investments Commission (ASIC). Branch operations in Australia will usually require an Australian Registered Body Number (ARBN).

Business and tax registrations

All businesses operating in Australia are required to have an Australian Business Number (ABN) issued by the Australian Taxation Office (ATO). On average registration for an ABN will take up to two weeks for the ATO to process, except where non-resident entities or individuals are involved. In these cases, additional identity verification processes apply which can extend the processing time of applications.

There may be other business registrations required such as GST and PAYG Withholding which can be obtained at the same time, or separately to, the ABN application.

A GST registration is required for businesses with GST turnover (typically being the annual business turnover) of $75,000. However, a business can also choose to register for GST voluntarily.

A PAYG Withholding registration is required for remitting tax withheld from payments to employees, other workers and businesses that do not quote their ABN. Registration is required prior to the first payment you are required to withhold from.

For income tax purposes, businesses will also be required to register for a Tax File Number (TFN) with the ATO.

Employers who provide certain non-cash benefits to employees will also be required to be registered for Fringe Benefits Tax. Fringe benefits could include provision of entertainment (such as staff social functions), provision of a motor vehicle, payment of private expenses, provision of rent-free accommodation and interest free loans. An employer is required to be registered if they are liable for FBT.

Payroll tax is a state tax, with employers required to be registered in each state/territory that they are liable for payroll tax. Payroll tax is determined based on the employer’s total Australian taxable wages (including non-cash benefits).

There are also specific lodgement obligations in respect of these tax registrations. Please refer to section 4 ‘What lodgements will I need to submit?’ for further details.

What tax rates apply?

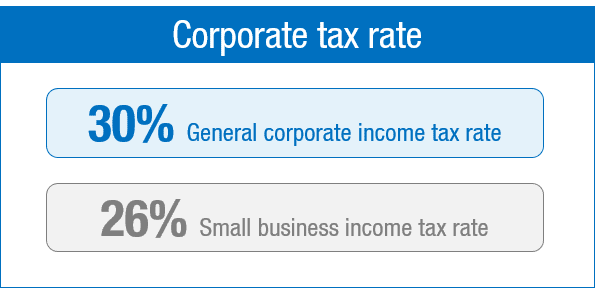

The general company tax rate for income tax in Australia is 30%. However, small-to-medium companies are taxed at 26% with the tax reducing to 25% by FY22.

Companies are required to pay their income taxes in instalments throughout the year. These instalments are paid either monthly or quarterly.

There are also withholding tax obligations in respect of dividends, interest, and royalties being paid to foreign residents. Such withholding tax applies to dividends generally at 0% or 30%, interest at 10% and royalties at 15%. However, these rates may be reduced by tax treaty arrangements.

Most sales in Australia are subject to GST of 10% of the value of the sale. However, sales that qualify as being GST-free or input taxed are exempt from GST.

Australia has a progressive personal income tax system, with the tax rates ranging from 0% up to 47%.

Corporate tax

The general company tax rate in Australia is 30% unless the company is a small-to-medium company.

A company is generally a small-to-medium company if its annual turnover is less than $50m. Small businesses are currently taxed at 26%, with the tax reducing to 25% by FY22.

Withholding taxes

Withholding tax applies to dividends, interest, and royalties being paid to foreign residents. The withholding tax rates are generally 0% or 30% for dividends, 10% for interest and 15% for royalties. These rates may be reduced by tax treaty arrangements between Australia and the country of the foreign resident.

The 0% rate for dividends applies to dividends from ‘tax paid’ profits. These are termed ‘franked’ dividends.

Goods and Services Tax (GST)

The GST rate in Australia is 10% of the value of sale. This GST rate is applicable to all sales made in Australia unless they are GST-free or input taxed. Sales that qualify as being GST-free or input taxed are exempt from GST.

GST is generally payable by the supplier and is included in the price of the goods or services being supplied.

Fringe Benefits Tax (FBT)

Fringe benefits tax is a tax payable by employers based on the value of non-cash benefits provide to employees. The FBT year applies from 1 April to 31 March. The fringe benefits tax rate is currently levied at 47% of the grossed-up value of the fringe benefits provided during the FBT year. In principle, the ‘gross up’ takes the cost of the benefit and grosses it up to the equivalent pre-tax income that an employee would have needed to earn to be able to have acquired the same benefit.

There various FBT exemptions and concessions available.

Payroll Tax

Payroll tax is levied in all states/territories in which the employer pays taxable wages, including non-cash benefits, above the relevant threshold.

Each state/territory has its own payroll tax rates and annual thresholds which vary year-on-year. The payroll tax for each state is on average 5% of the taxable wages exceeding the annual threshold. The thresholds vary from state to state, with the lowest being $650,000 in Victoria and the highest being $2,000,000 in ACT.

Payments to independent contractors are usually considered ‘taxable wages’ for payroll tax purposes.

What lodgements will I need to submit?

Key tax lodgements include an annual income tax return, and a periodic (monthly, quarterly or annual) activity statement to report PAYG withholding and GST, income tax instalments, Fringe Benefits Tax instalments and some other taxes.

Australian registered companies are required to notify ASIC of changes in their registration details and pay an annual fee. Foreign companies may also need to lodge audited financial statements.

Large entities which are part of a group with annual global turnover of AU$1 billion or more will also be subject to additional reporting requirements under CbC reporting regime.

Branches with an ARBN will need to lodge their parent entity’s annual financial statements with ASIC.

There are other lodgement obligations that can arise in specific situations.

Income tax

Whether you have set up a private company, public company or branch of a foreign entity in Australia, you will be required to lodge an annual income tax return.

The default reporting date is for the year ended 30 June. This can be changed on application to the ATO, for example to align with a foreign parent company’s year end.

Income tax returns are due on the 15th day of the seventh month after year end, for 15 July for a 31 December year end. Extended due dates are provided for 30 June year ends.

Activity statements

Activity statements are forms which taxpayers must submit to the ATO to report on various tax obligations, including:

- Goods and Services Tax (GST)

- Pay As You Go (PAYG) Withholding

- PAYG Instalments (income tax)

- Fringe Benefits Tax (FBT) instalments

- Wine Equalisation Tax (WET), and

- Luxury Car Tax (LCT).

If an entity is registered for GST, the reporting and payment cycle of activity statements will vary based on its GST turnover:

- Monthly: GST turnover is $20 million or more

- Quarterly: GST turnover is less than $20 million, and you have not been advised by the ATO that you must report monthly, or

- Annually: GST turnover is less than $75,000.

If you are uncertain whether you will need to register for GST, please refer to section 2 ‘What registrations will I need?’.

Similarly, PAYG Withholding reporting and payment cycles will be dependent on whether entities are ‘Small Withholders’, ‘Medium Withholders’ or ‘Large Withholders’, resulting in quarterly, monthly or twice weekly lodgement obligations, respectively.

PAYG Instalments are paid monthly for large taxpayers and quarterly for most smaller taxpayers. FBT instalments are also generally paid quarterly.

Additional lodgements for employers

Where an entity has employees, a number of lodgement obligations will arise.

Employers who provide certain non-cash benefits to employees will be required to lodge a Fringe Benefits Tax (FBT) return with respect to each FBT year (1 April to 31 March).

Payroll tax is state tax arising where wages paid by employers exceed specified threshold amounts. Payroll tax obligations vary between states and territories in terms of applicable thresholds, these also vary from state to state, with the lowest being $650,000 in Victoria and the highest being $2,000,000 in ACT.

Employers are also required to collect pay as you go (PAYG) Withholding on amounts paid to employees. Where an employer is registered for PAYG Withholding, they must report total amounts withheld in their activity statements (refer to ‘Activity statements’ section above).

Employers are also obligated to report employee salaries and wages, PAYG Withholding and superannuation contributions through Single Touch Payroll (STP). Employers are required to utilise STP-enabled payroll or accounting software which will automatically report this information to the ATO whenever payroll is run. STP is not required to be on a specific cycle and will follow the employer’s own pay cycle.

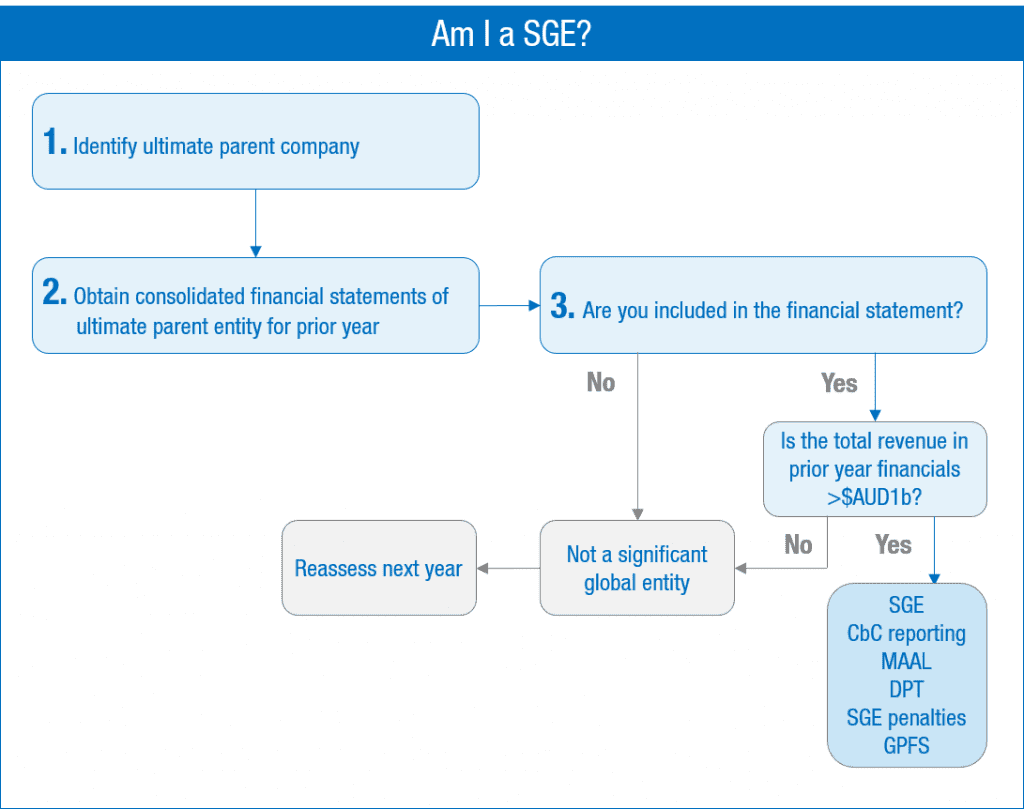

Significant global entities

Entities that are part of an accounting consolidated group with more than AU$1 billion in global annual turnover are considered a “significant global entity” (SGE).

SGEs are subject to an additional reporting obligation collectively referred to as Country-by-Country reporting.

SGEs will be required to lodge the following documents which contain detailed information regarding the entity’s international related party dealings:

- CbC report

- Master file, and

- Local file.

SGEs will be subject to significant penalties of up to AU$555,000 for late lodgement of any tax obligations, not only those applying specifically to SGEs.

Please refer to section 12 ‘What are the special rules for larger multi-nationals?’ for more information on SGEs.

Audited financial statements

Large proprietary companies are required to lodge audited financial statements, prepared in accordance with approved accounting standards, with ASIC.

A company is classified as large if it meets two of the following three criteria:

- Consolidated gross operating revenue more than $50 million a year

- Consolidated gross assets more than $25 million at year end, and/or

- Number of employees at year end is more than 100 for that entity and all controlled entities.

The proprietary company is otherwise categorised as small.

Small foreign controlled companies are required to prepare an audited financial report for lodgement with ASIC unless they obtain one of the following exemptions:

- Where their results are included in consolidated financial report lodged with ASIC by a registered foreign company or an Australian company, or

- Where the company obtains relief from ASIC before the commencement of the financial year, or within three months of incorporation in the first year.

Please refer to section 8 ‘Will I need to get an audit?’ for more information on audited financial statements.

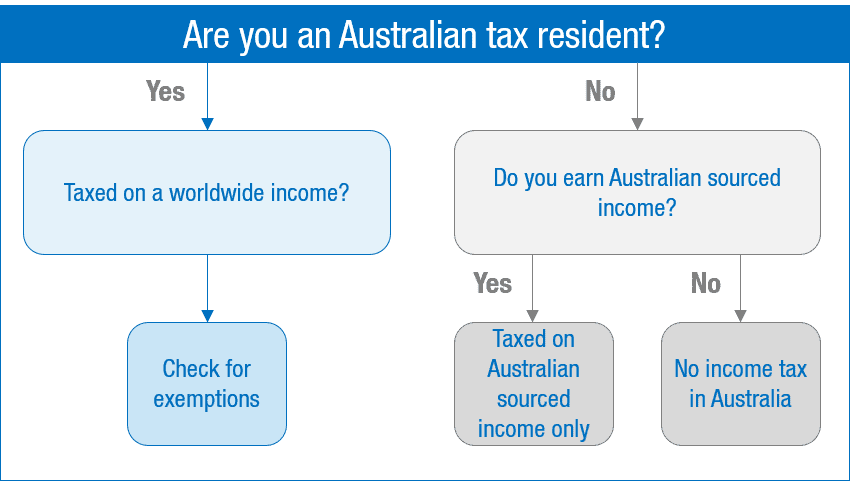

Will I be subject to income tax?

All Australian registered companies will be subject to income tax on their worldwide income. This is subject to some exemptions for income derived from foreign subsidiaries and branch operations (a participation exemption).

Branches of foreign companies will be subject to income tax on the profits from the Australian branch if they have a permanent establishment in Australia based on Australia’s domestic laws and any relevant tax treaty arrangement.

Assessable income

As a general rule, Australia will tax all Australian residents on their worldwide income and capital gains. Australian resident taxpayers include:

- Companies registered in Australia

- Companies that are registered overseas, but have their central management and control in Australia

- Trusts that have an Australian resident trustee at any time during the income year

- Trusts that have their central management and control in Australia at any time during an income year, and

- Individuals who are resident in Australia for tax purposes.

Certain types of income derived by Australian resident companies will be exempt from income tax. For example, exemptions from Australian income tax may apply to:

- Dividends received from wholly owned subsidiaries

- Profits of a foreign branch / permanent establishment of the Australian company, and

- Capital gains from the sale of shares in wholly-owned foreign subsidiaries.

For non-residents, Australia will tax:

- All net profits that are “attributable” to an Australian branch. These are generally the profits derived from the activities carried out by the branch in Australia, and

- Any Australian sourced income.

If income that is taxed in Australia is also taxed in a foreign country (i.e. there is double tax), Australia has a foreign tax offset system which may reduce the tax payable in Australia. If there is a double tax treaty between Australia and the country that has also levied tax on the relevant income, the double tax treaty may provide some relief from double tax.

Treatment of tax losses

Losses that an Australian taxpayer derives from trading may be carried forward indefinitely. These carried forward losses of a taxpayer may be offset against future operating profits of that taxpayer, if that taxpayer can pass certain tests. The tests that apply vary depending on what entity the taxpayer is.

For example, companies need to pass one of the following tests:

- The continuity of ownership test – broadly this requires that the same individuals have a majority ultimate beneficial ownership interest in the company from the start of the year that the losses are first incurred, until the end of the year in which the losses are applied, or

- The business continuity test – this requires that a company be carrying on the “same”, or a “similar” type of business in the year that it is intending to recoup the losses as it did just before it failed the continuity of ownership test.

The test that a trust must pass to apply carried forward losses varies depending on the type of trust.

A fixed trust must pass the ‘50% stake test’ and the ‘income injection test’. A non-fixed trust must pass the ‘control test’ and the ‘patterns of distributions test’ in addition to the 50% stake test and the income injection test.

Will I need to pay GST?

GST is a broad-based consumption tax that applies to the supplies of most goods and services. The GST rate is 10%. Businesses are required to remit GST to the ATO on supplies that they make, and are generally entitled to claim a credit for GST included in the price of acquisitions that they make.

A tax invoice needs to be issued for supplies that are subject to GST. A tax invoice is an invoice that includes specific details set out in the GST laws.

There are special rules for international transactions including the import or export of goods, supplies of services to non-residents and supplies of intangibles (such as software) by non-residents.

The GST implications of cross border transactions, including with related parties, is something we would recommend that specific advice be sought on.

General GST matters

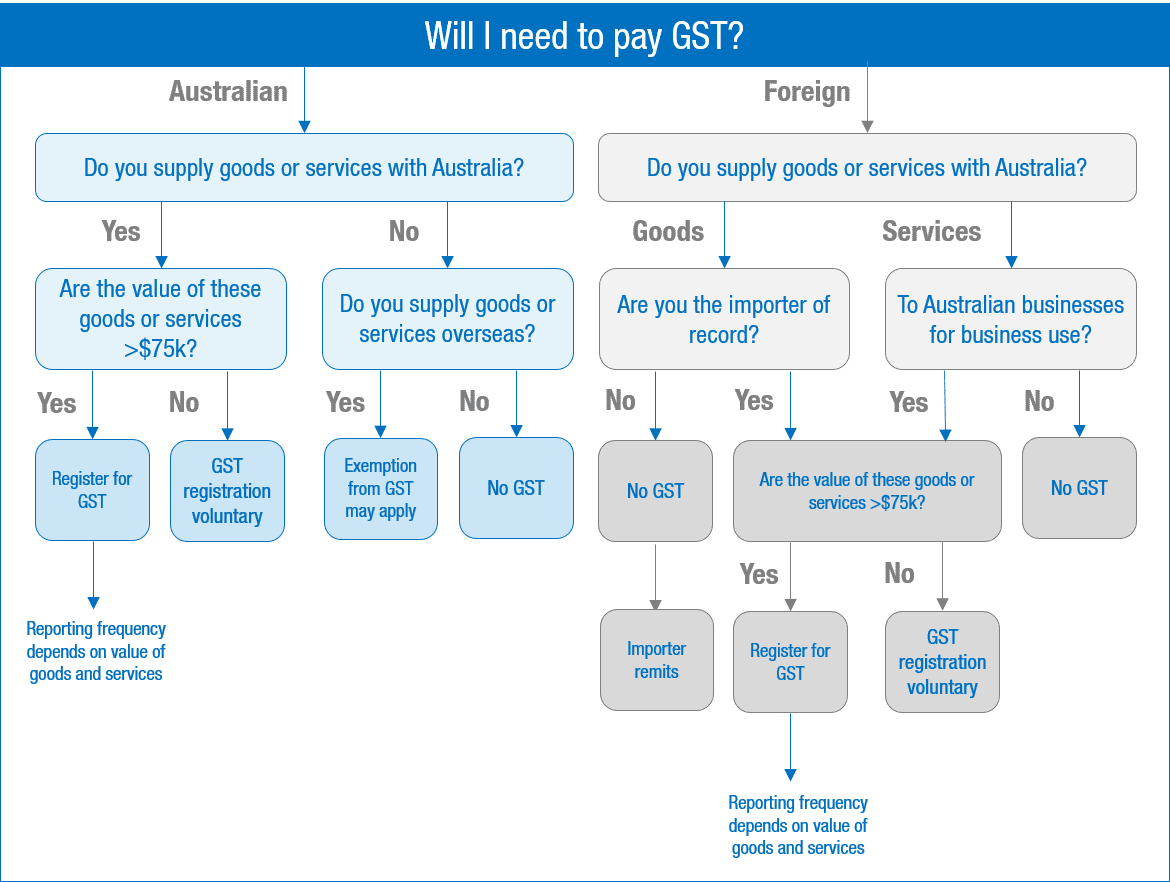

GST is payable on ‘taxable supplies’. To constitute a taxable supply, the supply must be:

- For consideration

- Made during furtherance of an enterprise

- Connected with Australia, and

- Made by a supplier who is registered or required to be registered for GST.

For overseas businesses transacting in Australia or with Australian customers, the key issue will be the connection with Australia.

The supply of goods will generally be connected to the jurisdiction where the goods are supplied. Care needs to be taken when importing goods to Australia as the importer of record will also carry the GST obligations on import.

Real property will relate to the jurisdiction in which it is located.

Services will generally be connected to the jurisdiction where the people rendering the services are located. If these people are in Australia, the supply will relate to Australia.

For non-residents making supplies of services to Australian businesses, there is an automatic reverse charge arrangement that can apply to shift the GST obligations to the Australian business.

Registered entities will obtain a credit for GST paid on most acquisitions where the items acquired are used in the course of their business.

A registered business must lodge GST returns either monthly or quarterly via a BAS. The net GST liability (GST payable, less GST input tax credits) is paid to the ATO at the same time.

Some supplies, such as financial supplies and residential rent, are ‘input taxed’. Input taxed supplies are not subject to GST. However, the supplier is not entitled to a refund of the GST paid on acquisitions that relate to making input taxed supplies.

There is also a limited range of GST-free supplies where GST is not required to be charged. Supplies of food (as defined) are GST free. The supplier is entitled to a refund of GST paid on acquisitions of GST-free supplies.

For entities registered for GST, a ‘tax invoice’ with the required information must be issued for each taxable supply. There are specific requirements relating to currency conversions where the consideration is denominated in a foreign currency.

There are no state based sales taxes.

Import and export

GST is payable on the importation of goods. The Australian Customs Service acts as a collections agent, and the GST needs to be paid before the goods are entered for use or consumption in Australia.

Where the imported goods are to be utilised in a business, a GST registered business will generally be entitled to claim a credit for the GST paid on importation. Subject to meeting specific eligibility criteria, a business can register for the ‘GST Deferral’ scheme which allows it to defer paying the GST on import until lodgement of the activity statement with the corresponding credit is claimed, thereby removing the cashflow impact on GST on importations.

Export sales are generally GST free. Likewise, the supply of services for consumption outside of Australia is generally GST free, but the terms of intercompany transactions should be reviewed from a GST perspective to confirm the GST treatment.

E-commerce

From 1 July 2018, GST is levied on “low value” imported goods, that is goods with a value of A$1,000 or less. This change is targeted at online retailers. An exception may apply where the goods are supplied to Australian entities registered for GST.

There are specific rules in the application of GST to inbound intangible supplies, including digital supplies (software downloads, SAAS, etc) has also changed. GST is levied on B2C intangible supplies where the customer is located in Australia, but not on B2B intangible supplies on the rationale that the business would claim a corresponding input tax credit so the transaction is revenue neutral.

Where sales are made via an electronic distribution platform (such as many of the common online e-commerce platforms), the GST obligations will sit with the EDR rather than the business that is making the actual supply.

Registration options

Two registration options are available to non-resident businesses. “Simple registration” allows the business to remit the GST it has charged to the ATO but prevents it from claiming credits for acquisitions it makes. To claim credits the business needs to complete the normal registration process, which involves being issued an ABN. This may also be appropriate for non-residents that are making significant acquisitions from Australia that are subject to GST. In the absence of registering, the GST would be a cost.

It can be possible for a non-resident to enter into an optional reverse charge agreement with an Australian customer to shift the GST obligations to the customer. This does not change the customer’s overall GST position and removes the obligation for the non-resident to register for GST.

GST reporting

GST is reported to the ATO on the monthly or quarterly activity statement. Payment is also made at this time.

Please refer to section 4 ‘What lodgements will I need to submit?’ for more information on BASs.

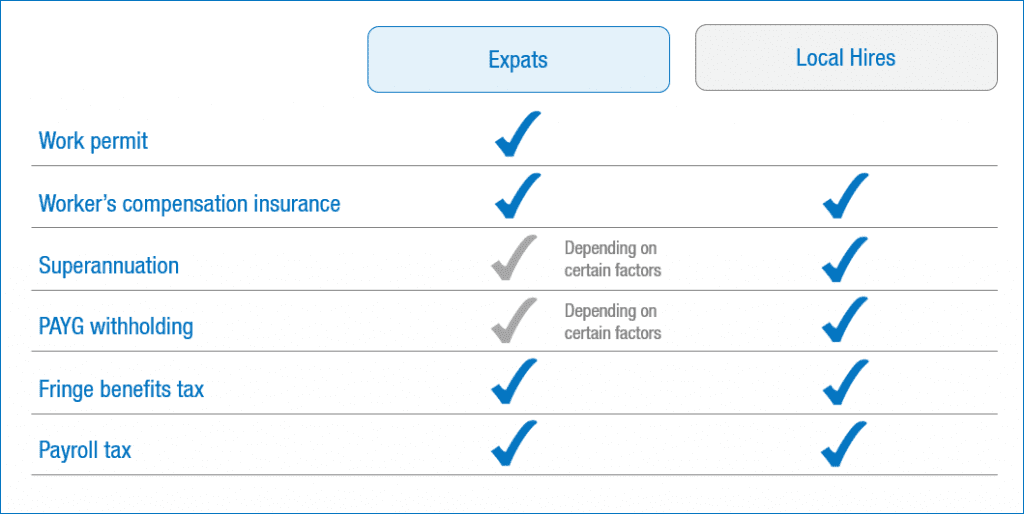

What are an employer’s employee related obligations?

If an employer is going to have employees in Australia, either local hires or expatriates, a series of tax and other obligations will arise.

Tax (termed PAYG Withholding) is required to be withheld from payments to employees. There are some exceptions, such as where the employee satisfies the short stay exemption in a tax treaty.

Superannuation (pension) contributions are required to be made by an employer on behalf of the employees. This is currently set at 9.5% of remuneration as a minimum. Some expatriate employees may be able to be exempted from the Australian superannuation system.

Non-cash benefits provided to employees (for example, health insurance, accommodation, use of a car, entertainment) may be subject to a fringe benefits tax (FBT). FBT is imposed on the employer.

A state-based payroll tax is payable if salary and wages paid to employees in that state exceed a threshold. The thresholds vary from state to state, with the lowest being $650,000 in Victoria and the highest being $2,000,000 in ACT.

Employers will also likely require a workers’ compensation insurance policy in each state where they have employees.

Expatriate employees will require a special visa to work in Australia. The visa classes vary depending on the role, industry and duration of the stay, amongst other factors.

Australia has strong employment laws and engaging an Australian employment law specialist to assist with drafting or reviewing employment contracts is recommended.

PAYG Withholding

Employers are required to register with the ATO for PAYG Withholding. Employers will withhold and subsequently remit to the ATO a portion of the salary paid to employees. The tax collected by the employer is known as Pay as You Go (PAYG) withholding. An employer will be subject to penalties for failing to withhold and remit the appropriate level of PAYG tax, or for late payment of PAYG tax, to the ATO.

At the end of each financial year, an employer is required to provide their employees with a ‘PAYG Payment Summary’, which shows their gross salary, how much PAYG was withheld and other specific payroll related items.

Employers are also obligated to report employee salaries and wages, PAYG Withholding and superannuation contributions through Single Touch Payroll (STP). Employers are required to utilise STP-enabled payroll or accounting software which will automatically report this information to the ATO whenever payroll is run. STP is not required to be on a specific cycle and will follow the employer’s own pay cycle.

Superannuation Guarantee Charge (SGC)

Employers are required to contribute a prescribed minimum level of superannuation support in each quarter for each of their employees. The minimum contribution is currently 9.5% of an employee’s ordinary times earnings (including commissions, bonuses and allowances). The minimum contribution will increase to 12% progressively over the coming years.

Employer must make the superannuation contributions within 28 days of the end of each quarter and notify their employees within 30 days of their contributions being made.

If an employer sends an Australian employee to work overseas temporarily, the employer must continue to pay super contributions in Australia for them. The overseas country may also require an employer to pay super (or an amount equivalent to super). However, Australia has bilateral agreements with some countries which would exempt an employee from paying the super in that overseas country.

In the alternative, an employer may not need to pay superannuation contributions in respect of expatriate/non-resident employees where their country of residence has entered into a specific bilateral social security agreement with Australia.

If an employer fails to pay the required amount they are subject to a superannuation guarantee charge (SGC) which is paid to the ATO and the superannuation payment becomes non-tax deductible.

Fringe Benefits Tax (FBT)

Where an employer provides non-cash benefits to an employee, their family or other associates of that employee, FBT may need to be paid by the employer in respect of those benefits. Examples of fringe benefits include allowing an employee to use a car for private purposes, paying an employee’s gym membership and reimbursement of a private expense incurred by an employee, such as school fees.

Employers must self-assess the amount of FBT they have to pay and lodge a FBT return at the end of each FBT year (1 April to 31 March). When working out their FBT liability, employers will need to ‘gross up’ the taxable value of benefits provided to their employees.

For example, the FBT on a GST free expense paid on behalf of an employee (e.g. health insurance) of $1,000 would be $886 ($1,000 x 1/(1- 47%) x 47%). The reason for the gross up of the benefit is that the employee on the top marginal tax rate must earn $1,886 to have net income of $1,000 after income tax of $886 ($1,886 x 47%) to pay for the benefit if it came out of their salary.

In effect, employers pay the employee’s income tax on fringe benefits, with the assumption that the top marginal tax rate applies. Accordingly, before negotiating an employee’s package you should ensure that you are aware of the full cost of the package, including FBT, to the employer.

There are limited opportunities to package expatriate employee’s remuneration, including some concessionally taxed benefits, to minimise FBT and income tax.

Payroll tax

An employer may also be required to pay payroll tax in respect of payments to their employees.

Salary and wages, bonuses, some allowances, the taxable value of fringe benefits and superannuation contributions are all ‘taxable wages’ for payroll tax purposes. Payments to independent contractors are also subject to payroll tax unless an exemption applies.

The payroll tax rates and thresholds differ depending on the laws in each state and territory. The payroll tax for each state is on average 5% of the taxable wages exceeding the annual threshold. The thresholds vary from state to state, with the lowest being $650,000 in Victoria and the highest being $2,000,000 in ACT.

Each state and territory has grouping rules, which operate to group ‘connected’ entities so that they are not able to access multiple payroll tax thresholds across the states and territories.

Workers' compensation insurance

Employers are required to carry workers’ compensation insurance for its employees in respect to work-related injuries. Once a business employs staff in Australia, workers’ compensation insurance must be taken out in each state/territory the company has employees. The cost of this insurance will range from 1% to 10% of payroll costs, depending on the nature of the business.

Work permits and visas

An expatriate travelling to Australia for business purposes must obtain appropriate employment authorisation (Temporary Skill Shortage (TSS) Visa subclass 482).

In March 2018, the TSS Visa replaced the 457 visa and introduced new requirements including tightened English language requirements and a requirement for applicants to have at least two years’ experience in their skilled occupation.

Companies operating in Australia, or those in other countries wishing to establish operations in Australia, can sponsor individuals on the TSS Visa. Employers who are already approved standard business sponsors for the 457 Visa can sponsor skilled overseas workers under the TSS Visa by lodging a renewal form prior to the expiry of their existing sponsorship.

The TSS Visa allows an expatriate to work in Australia for:

- Two to four years (under the Short-term stream), and

- Up to four years with the possibility of applying for permanent residency (under the Medium-term stream).

There is an additional stream called the ‘Labour Agreement’ stream, which applies where the employer has a labour agreement with the Australian government and allows an expatriate to work in Australia for up to four years.

Obtaining temporary work authorisation under the TSS Visa involves a three-step process:

- A sponsorship application by the employer

- A nomination application for a skilled position by the employer, and

- A visa application by the proposed employee.

Nominations:

- Are restricted to a list of occupations that is significantly smaller than the list of occupations approved under the previous 457 Visa

- Extend to activities in regional areas including occupations relating to farming and agriculture, and

- Must meet salary and employment condition related requirements.

The necessary applications are lodged and processed in Australia with the Department of Home Affairs. Prior to lodgement, it will be necessary to gather all the relevant documentation relating to the application. The usual time to assemble the documentation is approximately three to four weeks.

Once the application is lodged with the Department of Home Affairs, the processing time frame can be up to eight weeks (however processing times may vary depending on the stream). Complete nomination applications are likely to be processed more quickly. Incomplete applications might be delayed or refused after two days if there is insufficient information provided to demonstrate that requirements are met.

This application process is normally undertaken in conjunction with a visa/migration specialist advisor.

A visa holder cannot change conditions of employment without prior approval from the Department of Immigration.

Terms of employment

Australia’s industrial and workplace relations laws have undergone significant change in recent times through government initiatives designed to make the labour market more flexible and efficient. In establishing a presence in Australia, care should be taken to ensure that any terms of employment are in accordance with the relevant Australian legislation.

We recommend that employment contracts be reviewed by a specialist employment lawyer to ensure compliance with the Australian legal requirements.

What issues should an expatriate employee consider?

Income tax

For Australian tax purposes, individuals living and working in Australia will be categorised as either ‘resident’, or ‘non-resident’. The imposition of tax on an individual will differ depending on their tax residency status.

The most fundamental distinction is that a resident will be subject to Australian income tax on their worldwide income (including capital gains), whilst a non-resident is subject to Australian income tax on Australian sourced income only. Further, resident individuals will be entitled to the tax-free threshold, however they will also be liable to pay the Medicare levy of 2%.

Expatriate employees may be classified as temporary residents (regardless of whether they are resident or non-resident under the general rules). As a temporary resident, they will be taxed in Australia on their Australian sourced income and all remuneration (regardless of source) for employment services rendered whilst they are a temporary resident.

Individuals should review their personal investments and other income sources and assets prior to becoming a resident (or ceasing to be a resident) of Australia. This will help them to determine the potential tax exposure of a change in tax residency and establish whether there are any planning opportunities.

Work permits and visas

An expatriate travelling to Australia for business purposes must obtain appropriate employment authorisation (TSS Visa). The process for obtaining this type of visa is outlined above.

Expatriates moving overseas should also consider whether they need to obtain a similar work permit or visa to enable them to work in the foreign country of their choice.

Private health insurance

Expatriate employees may not be eligible for medical cover under the National Medicare Scheme while working in Australia.

Australia has health care agreements with some countries. These countries are the United Kingdom, New Zealand, Italy, Netherlands, Malta, Sweden, Ireland, Belgium, Slovenia, Norway and Finland. Residents of these countries are entitled to limited access to Medicare, but only in emergency situations.

It is therefore necessary for expatriates on temporary business visas to consider taking out private health insurance to cover themselves in the event of sickness or a medical emergency even if partial health cover is available via one of the health care agreements mentioned above. Sometimes this is a requiremnet of obtaining the visa.

There are various private health funds operating throughout Australia which provide such insurance.

Medicare levy surcharge (MLS)

Resident individuals are liable to pay a Medicare levy based on the amount of their taxable income for the income year. The Medicare levy rate for the 2019/20 year is 2% of taxable income.

Individual taxpayers on higher incomes, who do not have adequate private patient hospital insurance for themselves and their dependants, may be liable for an additional Medicare levy surcharge of 1%, 1.25% or 1.5%, depending on their income level. For instance, individuals who earn more than $90,000 in the 2019 income year and do not have private health insurance are potentially liable for the MLS. Higher thresholds apply where dependants are involved.

If an individual cancels their private health insurance when moving overseas, they may still be liable for the MLS if they remain an Australian resident and their income exceeds the relevant threshold. In these circumstances, the individual should contact their health fund to determine whether any saving in premiums from cancelling or suspending health cover would outweigh the potential MLS payable.

Superannuation

When an expatriate moves overseas, their superannuation in Australia will remain subject to the same rules even if they are leaving Australia permanently. This means they will not be able to access their superannuation until they reach their preservation age and retire or satisfy another condition of release.

If an expatriate is planning on moving permanently or indefinitely to New Zealand, they may be able to transfer their super to a New Zealand KiwiSaver scheme from a participating Australian super fund.

An individual moving to another country may be able to secure the release of their superannuation but a tax liability will arise.

Will I need to get an audit?

Australian registered companies are required to prepare audited annual financial statements and lodge these with ASIC if the company is a large proprietary company. Small Australian owned proprietary companies do not need an audit.

A company is a large proprietary company if it meets two of three criteria, which are: employing more than 100 full time equivalent employees; $50M or more annual turnover; and $25M or more gross assets.

Foreign owned companies are required to prepare audited annual financial statements and lodge these with ASIC. However, foreign owned companies that are also small proprietary companies can apply to ASIC for an exemption.

The large proprietary tests

The reporting requirements of proprietary companies and registered foreign companies depend on whether the company is defined as large or small under the Corporations Act.

A company is classified as large if it meets two of the following three criteria:

- It has a consolidated gross operating revenue of more than $50 million a year

- It has consolidated gross assets of more than $25 million at year end, and/or

- Its number of employees at year end is more than 100 for that entity and all controlled entities

The proprietary company is otherwise categorised as small.

The Corporations Act sets out the requirements for a company to prepare a financial report for lodgement with ASIC and the need to have the report audited. Once lodged with ASIC the financial report is available to the public.

Special rules for foreign owned companies

Small foreign controlled companies are required to prepare an audited financial report for lodgement with ASIC unless they obtain one of the following exemptions:

- Where their results are included in consolidated financial report lodged with ASIC by a registered foreign company or an Australian company, or

- Where the company obtains relief from ASIC before the commencement of the financial year, or within three months of incorporation in the first year.

Accounting records

The Corporations Act requires records to be kept for seven years from the date of the transaction.

Where statutory accounts are not required the directors are still required to maintain accurate accounting records to explain the company’s financial transactions and financial position and to enable statutory accounts to be prepared if required. Management accounts are necessary for tax and management purposes and to allow the directors to monitor compliance with their fundamental obligation under the Corporations Act to ensure the company can meet its debts as and when they fall due.

A company must have a fixed accounting period of 12 months except in the first year, or for a transitional year where a change occurs in the balance date of the company.

The default balance date is 30 June, but this can be change, for example to align with the parent company’s year end.

What incentives are available?

The Research and Development Tax Incentive is available to Australian companies conducting experimental research and development activities that may benefit the wider Australian economy. Companies that satisfy the eligibility criteria may be entitled to a cash refund of up to 43.5% of the costs incurred in conducting the R&D activities.

The Accelerating Commercialisation Grant can provide Australian businesses with up to AUD $1 million of matched funding to take a novel product, process or service to market. Unlike the R&D Tax Incentive, this is a competitive grant with a limited number of applicants approved each year.

Most States provide incentives for businesses to employ new workers. Depending on the size of the business, the incentive could be a cash rebate or a reduction of the business’ overall payroll tax liability.

The Export Market Development Grants (EMDG) scheme encourages export-ready Australian businesses to increase international marketing and promotion expenditure by reimbursing up to 50% of eligible expenses such as marketing consultants, trade fairs, advertising and marketing visits.

Depending on the business’ size, location and industry, there are numerous other Federal and State Government grants and incentives that may be available.

R&D Tax Incentive (R&DTI)

The R&DTI is available to Australian companies conducting experimental research and development activities that may benefit the wider Australian economy. To qualify, the company must be conducting at least one “core R&D activity” during the year that demonstrates the following:

- The aim of the activity is to generate new knowledge in the form of new or improved products, processes or services.

- The outcome of the activity could not have been known in advance of conducting the activity, and

- A systematic progression of work based on the principles of established science.

For companies with an aggregated turnover of less than AUD $20 million, the incentive is in the form of a 43.5% refundable tax offset. For all other companies, the tax offset is 38.5% and non-refundable.

The R&DTI is jointly administered by the ATO and AusIndustry. Claimants self-assess their eligibility and are required to keep detailed records of their R&D activities conducted during the year.

There are additional measures for Australian subsidiaries conducting R&D activities on behalf of a foreign parent company.

Accelerating Commercialisation (AC) Grant

The AC Grant provides Australian businesses with up to AUD $1 million of matched funding to take a novel product, process or service to market. To qualify, companies must:

- Have a novel product, process or service they wish to commercialise

- Be seeking to trade in an Australian state or territory other than the one the business is situated

- Be undertaking an eligible project, as defined by the Australian Government

- Own or have access to the beneficial use of any IP required for the project, and

- Not appear on the Workplace Gender Equality Agency list of non-complying organisations.

Unlike the R&D Tax Incentive, this is a competitive grant with a limited number of applicants approved each year.

Other incentives

Most States provide incentives for businesses to employ new workers. Depending on the size of the business, the incentive could be a cash rebate or a reduction of the business’ overall payroll tax liability.

The Export Market Development Grants (EMDG) scheme encourages export-ready Australian businesses to increase international marketing and promotion expenditure by reimbursing up to 50% of eligible expenses such as marketing consultants, trade fairs, advertising and marketing visits.

Depending on the business’ size, location and industry, there are numerous other Federal and State Government grants and incentives that may be available.

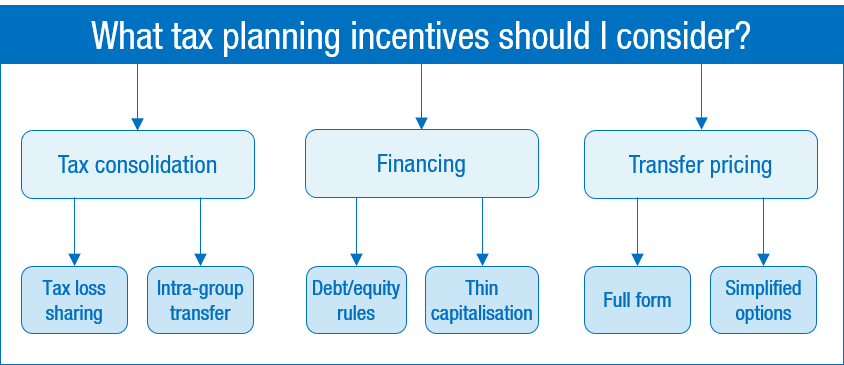

What tax planning should I consider?

Australia has strong transfer pricing laws and robust general anti-avoidance provisions, so much of the tax planning that may be appropriate in other jurisdictions will not be appropriate in Australia.

Nevertheless, overseas businesses should consider:

- The ideal structure to repatriate profits in a tax-effective manner

- The mix of debt and equity used to fund the Australian operations, as this will have an impact on the amount of interest expenses that can be claimed as a tax deduction, and

- Forming a tax consolidated group so that multiple entities operating in Australia can be treated as a single taxpayer, enabling the sharing of tax losses and facilitating intra-group transactions.

Tax consolidation

The tax consolidation regime allows wholly-owned Australian group companies (together with eligible trusts and partnerships) to consolidate for tax purposes.

Entry into the tax consolidation regime is not compulsory, but there is very limited group relief available for groups that choose to remain outside of the tax consolidation regime.

The rules may also apply to wholly-owned Australian subsidiaries of a foreign parent even when the Australian subsidiaries may not themselves be part of an Australian wholly-owned group of companies (i.e. the foreign parent has direct investment into two or more Australian subsidiaries). Such a scenario is referred to as a ‘multiple entry consolidated’ (MEC) group.

Entities that are part of a consolidated group are treated as one entity for income tax purposes and will lodge one income tax return that covers all members of the group. This will allow the losses of one group member to be offset against the assessable income of another entity within the group

Transactions between entities that are part of the same consolidated group are effectively ignored for income tax purposes.

However, entities that form part of a consolidated group for tax purposes are still separate legal entities. As such, they are still required to maintain separate accounts, records etc.

It should be noted that GST, FBT and PAYG Withholding tax are not included within the tax consolidation regime and will continue to be the responsibility of the individual entities in the group.

Separate grouping rules are available for GST.

Financing - debt vs equity

When reviewing your financing of the Australian operations, consideration should be given as to whether you wish to finance the entity with equity or debt. This decision is usually made in conjunction with the thin capitalisation rules outlined below.

When the funding of an entity will occur in part with debt, care should be taken to ensure that the debt instrument (e.g. a loan) will meet the tax definition of ‘debt’.

Factors such as the applicable interest rate (or interest free nature of the loan), term of the loan and existence of other debt or equity instruments can impact the classification of the loan. If a loan is determined to be equity, any interest will be treated as a dividend and not deductible.

Thin capitalisation

The thin capitalisation rules operate where the amount of debt used to finance the Australian operations exceeds certain limits. The rules can operate to disallow a proportion of the finance charges (e.g. interest) attributable to the Australian entity. If the entity is part of a tax consolidated group, the tests are applied to the overall group.

Broadly, the amount of debt used to finance the Australian investments will be excessive where it is greater than the safe harbour debt to equity ratio of 1.5:1.

Specifically, the thin capitalisation rules apply a test known as the ‘safe harbour debt test’, which requires that the company’s total average debt should not exceed 60% of the average value of Australian assets. Accounting standards are applied in calculating and measuring the value of assets (including revaluations) and liabilities. Additionally, from 1 July 2019, the valuation of assets for thin capitalisation purposes must be consistent with what is recorded in the financial statements of the relevant entity. This safe harbour test applies to all debt, not just foreign (related party) debt.

Where borrowings exceed the safe-harbour ratio, an alternate arm’s-length test can be applied. Essentially, the arms-length test will be satisfied if the borrowing could have been borne by an independent entity. There are strict criteria that must be satisfied to apply this test. A further alternative test is also available for outward investing entities based on 100% of their worldwide debt.

The thin capitalisation legislation also includes a de minimis threshold below which the thin capitalisation rules do not apply.

This test allows entities with ‘debt deductions’ (being interest and other debt costs) of less than $2 million to claim a tax deduction for the debt deductions without having to satisfy any of the thin capitalisation tests.

Notwithstanding the safe harbour limits, the ATO may challenge related party debt arrangements where the debt is not commercially realistic and at arm’s length through application of the transfer pricing provisions.

Due to the complexity of this area we would recommend that detailed advice and discussions be held prior to the finalisation of the capital structure of the Australian subsidiary.

Using an Australian holding company

Australia provides a number of exemptions for Australian holding companies with foreign investments and income.

An Australian holding company will generally not be taxable on the capital gain made on the sale of a foreign subsidiary. The Australian holding company would also not be taxable on dividends paid by the foreign subsidiary. By using the conduit foreign income mechanism, these foreign dividends can be passed through the Australian holding company to a foreign shareholder without triggering Australian income tax or withholding tax liabilities.

A non-resident shareholder in an Australian company will generally not be taxable on any gain made on the sale of the shares in the Australian company.

Non-residents are subject to Australian capital gains tax only where the assets are interests in Australian real property, or the business assets of Australian branches of a non-resident. Australian CGT also applies to ‘indirect Australian real property interests’, being non-portfolio interests in interposed entities (including foreign interposed entities), where the value of such an interest is wholly or principally attributable to Australian real property.

‘Real property’ for all these purposes is consistent with Australian treaty practice and extends to other Australian assets with a physical connection to Australia, such as mining rights and other interests related to Australian real property.

A ‘non-portfolio interest’ is an interest held alone or with associates of 10% or more in the interposed entity.

This means that it is only the sale of shares in a ‘land rich’ Australian company that would give rise to an Australian capital gains tax liability for a non-resident shareholder.

This should be contrasted to the situation of an Australian branch, where any gain on the sale of the assets of the Australian branch will be subject to tax in Australia.

Transfer pricing

Australia applies transfer pricing provisions which are based on the OECD guidelines.

The legislation seeks to ensure that Australian businesses deal with international related parties on arm’s length terms and conditions.

These provisions apply to all Australian businesses, regardless of the type of entity used. It therefore applies equally to an Australian branch of an overseas company (treated as a separate taxpayer) and an Australian subsidiary.

The Australian transfer pricing rules provide the ATO with broad powers to notionally reconstruct the financial results of a taxpayer and provide a legislative basis for applying ‘profit based’ approaches to calculate transfer pricing adjustments.

The key features of the Australian transfer pricing rules can be summarised as follows:

- It is a requirement to prepare contemporaneous transfer pricing documentation to support that international related party transactions have been conducted on arm’s length terms. Penalty protection will not be available if there is not contemporaneous documentation in place.

- Taxpayers that have international dealings with related parties that are more than $2 million need to lodge an International Dealings Schedule (IDS) with their annual income tax return The IDS is a detailed form requiring full disclosure of all international related party transactions, the main transfer pricing method that is applied to each transaction, along with a disclosure as to the level of specific transfer pricing documentation held for that transaction or dealing.

- Simplified transfer pricing documentation options are available to taxpayers with lower value and low risk international dealings where specific eligibility conditions are met.

- The ATO is relatively sophisticated in the transfer pricing area and in the last decade has implemented several programs which target taxpayers in a particular sector or with certain attributes. It does not only focus on large corporations but also has an active interest in the small to medium enterprise (SME) area.

The ATO is limited to a seven-year review period when making a transfer pricing adjustment. It is therefore in a taxpayer’s interest to ensure that its international related party dealings are conducted at arm’s length and that supporting documentation has been prepared and maintained from the outset.

What are the foreign investment restrictions?

Australia has limited restrictions on foreign investment and no exchange controls.

Under the Foreign Acquisition and Takeovers Act 1975 (Cth) (FATA), certain investments by foreign persons, foreign owned corporations or foreign governments may be restricted or subject to approval from the Foreign Investment Review Board (FIRB). FIRB examines foreign investment proposals and advises the Treasurer on the national interest implications. The Treasurer is responsible for making decisions on whether or not to approve foreign investment proposals. Generally, the Treasurer has 30 days to decide and the applicants will be informed of the decision within 10 days of it being made.

The restrictions and thresholds vary, depending on the type of investment, the relevant industry, the percentage of the asset or interest to be acquired, the dollar amount proposed to be invested and the identity of the foreign investor.

Some common investments that are subject to approval include:

- Acquisitions of substantial interest (20% or greater) in Australian businesses

- Investments in land and land rich entities

- Investments in agricultural land and agribusiness

- Investments in mining or production tenements, and

- Investments in sensitive businesses including media, telecommunications, transport and various military applications.

The foreign investment controls are significantly relaxed for non-government investors from Canada, Chile, China, Japan, Korea, Mexico, New Zealand, Singapore, Thailand and the US as these countries have Free Trade Agreements with Australia.

The thresholds that apply to different investments can be found at FIRB’s website firb.gov.au.

There are currently tighter restrictions on foreign investment due to the Covid situation. Details of these measures can be found at FIRB’s website firb.gov.au.

What are the special rules for larger multi-nationals?

Australia has implemented additional reporting obligations and targeted integrity measures for entities that are Significant Global Entities (SGEs). Broadly, an SGE is an entity which is part of an accounting consolidated group with more than A$1 billion in global annual turnover. SGEs can include large groups controlled by private companies, trusts and partnerships.

These reporting obligations and integrity measures include:

- Lodgement of Country by Country (CbC) reporting, which include lodgement of a Master File, a Local File and a CbC report with the ATO within 12 months of the end of the income year. The Master File and CbC report requirements are consistent with the OECD guidelines. However, Australia has implemented a different format from the OECD format for the Local File, being a transactional data focused XML schema.

- Provision of General Purpose Financial Statements (GPFS) with the ATO where not already filed with ASIC.

- The Multinational Anti-Avoidance Law (MAAL), which is designed to target inbound SGEs which derive Australian sourced income but have structured the arrangements such that the income is earned by a non-resident entity which is not subject to Australian income tax; and

- The Diverted Profits Tax (DPT), which allows the ATO to impose a penalty rate of tax of 40%, plus interest, on profits that are artificially diverted out of Australia through contrived arrangements.

In addition, SGEs are subject to substantial administrative penalties for failing to meet their tax obligations. Late filing penalties for any type of report could be up to A$555,000.

Important: An OECD local file will not be sufficient to discharge local file lodgement obligations in Australia as Australia has adopted specific reporting format and content requirements.

We can assist you with reviewing the business operation structures, the internal processes, risk management for the increased penalties and the level of documentation available to evidence the business arrangements.